[ad_1]

As mortgage charges proceed their ascent towards 6%, increasingly people are speaking housing market crash.

However excessive rates of interest aren’t actually a catalyst for a crash, particularly if the excessive charges aren’t actually excessive.

Emphasis on “actual,” as in inflation-adjusted. All the pieces has gone up in worth, and wages also needs to be rising.

This implies the next mortgage charge isn’t even a roadblock, or actually as unhealthy because it appears.

And since charges stay traditionally low, when you issue inflation, they might nonetheless be seen as a screaming deal.

Excessive Mortgage Charges Don’t Crash Housing Markets

I’ve stated it numerous occasions, and I’ll repeat it once more. Greater mortgage charges don’t mechanically decrease residence costs. Or decrease them in any respect.

If one goes up, the opposite doesn’t go down. And vice versa. It’s potential each can transfer in tandem, or reverse each other, based mostly on many different components.

So those that have been watching 30-year fastened mortgage charges completely surge from under 3% to practically 6% have to be beside themselves.

How may residence costs not fall, or on the very least, not proceed to rise? This is mindless.

Why would residence consumers proceed to pay such outrageous costs now that rates of interest aren’t at report lows?

A part of the reply is they need/want shelter, in order that they’re keen to pay “prime greenback” for it.

Another excuse is it’s nonetheless not that costly when you consider inflation and rising wages for these residence consumers.

The opposite key issue continues to be a provide/demand imbalance, with means too little stock out there to fulfill demand.

Oh, and there are many consumers paying all-cash for his or her residence buy, which has nothing to do with mortgage charges.

All of these items have stored the housing market buzzing by means of spring, seemingly defying the expectations of housing bears and naysayers.

Don’t Evaluate Immediately’s Housing Market to the One Previous the Nice Recession

There’s a saying that historical past doesn’t repeat itself, however it rhymes. The origins of that quote or comparable are arduous to find out.

However the basic thought is that we use the previous to foretell what is going to occur sooner or later. And we use the same occasion for route.

Relating to the housing market, anybody who’s skeptical of proper now’s wanting again to the Nice Recession.

Particularly, the housing market from round 2006 to 2008. Sadly, that’s a really excessive comparability, therefore its title.

The Nice Recession came about between 2007 and 2009, whereas the Nice Melancholy occurred between 1929 and 1939.

These had been each extreme financial downturns, and as such, had been spaced properly other than each other.

This implies the possibility of one other occasion of that magnitude anytime quickly is fairly low.

Nonetheless, we’ve loved many fruitful years currently, so a recession or downturn of some sort is definitely within the playing cards.

The query is how unhealthy will it’s this time round?

Ought to We Have a look at the Late Seventies and Early Eighties for Future Steering?

As an alternative of evaluating at the moment’s housing market to the one which preceded the Nice Recession, we would wish to look again a bit additional.

The housing market in 2006 was fueled by an abundance of acknowledged earnings and no-doc adjustable-rate mortgages, tons of money out mortgages, and zero down mortgages.

None of that’s current at the moment, although comparatively innocent hybrid ARMs just like the 5/1 ARM are starting to make extra of an look.

Now if we return so much additional in historical past, we would discover a higher instance for our historical past “rhyme.”

I’m speaking concerning the late Seventies and early Eighties, when inflation was tremendous excessive and mortgage charges spiked.

The previous timers love speaking about how excessive mortgage charges had been again then. They scoff at your 6% mortgage charge at the moment.

And so they have good motive to scoff – the 30-year fastened climbed as excessive as 18.45% in October 1981, per Freddie Mac information.

Only a few years earlier, it was as low as 9.01%, so mortgage charges actually doubled. And did so at very excessive ranges.

Whereas our mortgage charges are nonetheless ridiculously low by comparability, they’ve practically doubled as properly in only a matter of months.

Moreover, demographics are very favorable for residence shopping for, with 45 million Individuals hitting the first-time residence purchaser age of 34 between 2017 and 2027.

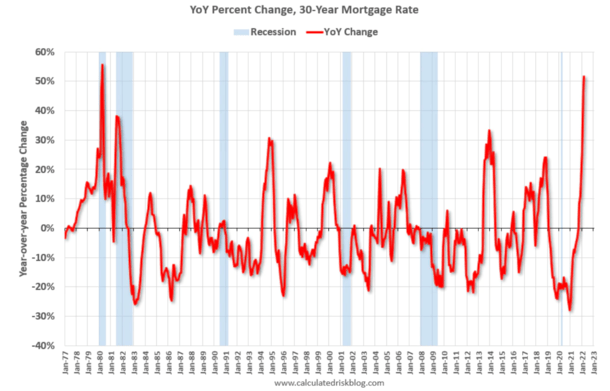

That is just like what was occurring again then, as Invoice McBride of Calculated Threat factors out.

As you possibly can see from his chart above, there’s been a really comparable year-over-year change in mortgage charges on a proportion change foundation.

The one massive distinction between then and now is perhaps stock. I say would possibly as a result of he doesn’t have the information, nor do I.

However we all know housing stock is at report lows at the moment, so chances are high at the moment’s housing market is much more insulated than the late 70s/early 80s market.

So what is going to occur to residence costs? Will we lastly get our massive, overdue crash?

Actual Residence Costs Could Fall, However Nominal Costs Could Not

Okay, so it is perhaps higher to check at the moment’s housing market with the one seen within the late 70s/early 80s.

That is smart given the inflation and rate of interest atmosphere, although bear in mind historical past doesn’t repeat itself, it merely rhymes.

This gives us with clues as to what occurs subsequent, however nothing definitive.

McBride’s take, based mostly on analyzing that point interval, requires a decline in each housing begins and new residence gross sales.

We may additionally see a rise in housing stock, although as talked about, it’s at the moment at report low ranges.

Right here’s the kicker – nominal residence costs won’t even go down through the subsequent “housing bust.”

By nominal, I imply costs that aren’t adjusted for inflation. In order that overpriced $500,000 residence is perhaps value $550,000 in a pair years.

That’s fairly wild while you have a look at how a lot residence costs have already risen.

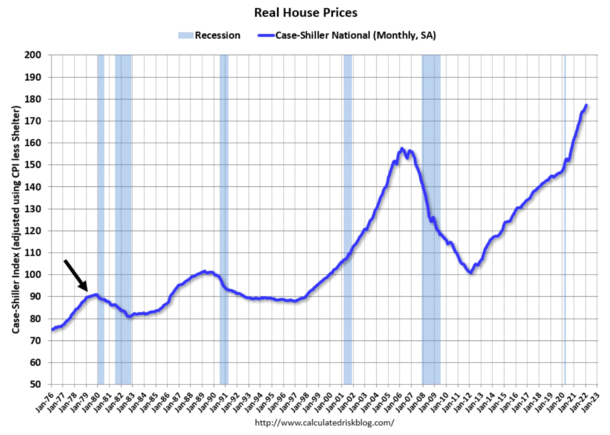

Nevertheless, actual residence costs (these adjusted for inflation) could decline, as they did from 1979 (after they peaked) till 1982.

Again then, they fell 11% in actual phrases, however nominal costs “elevated barely” on account of inflation.

In different phrases, chances are you’ll wish to mood your expectations with regard to an enormous housing market crash.

Sure, residence costs are “loopy excessive,” however so is the worth of every thing else.

And hundreds of thousands of Individuals are having fun with very low, fastened housing funds which are solely getting cheaper as costs and rates of interest rise.

So a flood of distressed gross sales and foreclosures seemingly isn’t within the playing cards because it was a decade in the past.

For these of you ready on the sidelines in search of a hearth sale, it could not occur.

And those that merely wish to purchase a house may additionally not see any main reduction.

This isn’t to say you need to panic-buy a home, however ready for some massive worth reduce won’t be a fantastic technique both.

[ad_2]

Leave a Reply